Table of Content

You may may be approved for a higher DTI ratio with strong credit scores or extra cash reserves. Home Possible Advantage offers qualified low- and moderate-income borrowers a conforming conventional mortgage with a maximum loan-to-value ratio of 97 percent. Home Possible Advantage mortgages can be used to buy a single unit property or for a “no cash out” refinance of an existing mortgage. Home Possible® is a Freddie Mac program designed to help borrowers with low-to-moderate incomes fulfill their dream of owning a home. It offers low down payments and has easier credit score requirements.

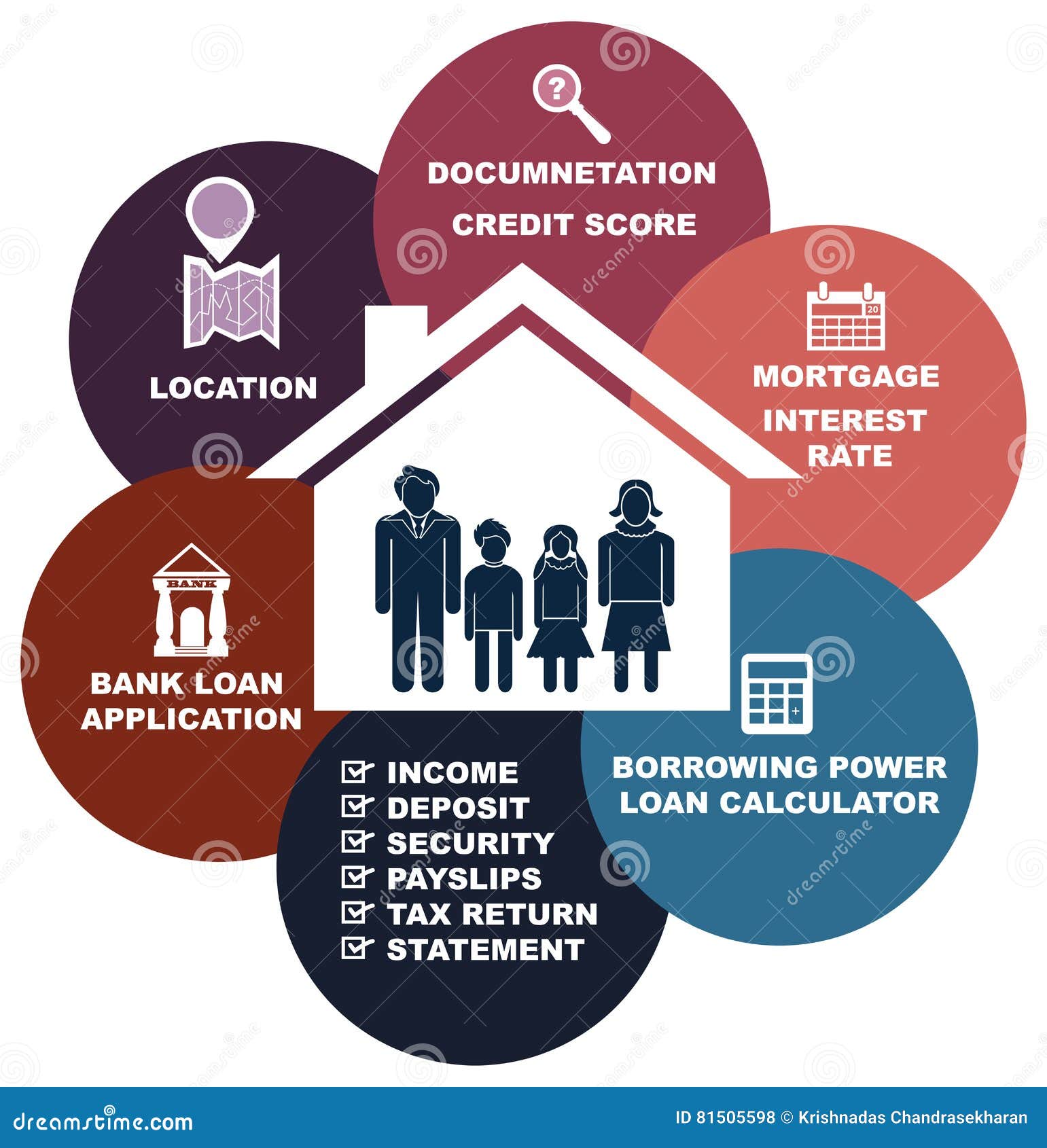

That’s why it’s essential to talk to your mortgage lender about which loan programs might be best for you. If you’re a first-time home buyer, there are several types of loans you can apply for when purchasing a home. Many of these loans are gratefully more forgiving on their eligibility to help first-time borrowers. Now let’s say you have other debt — maybe a car payment, a student loan, and credit card payments. Your lender might say you can only afford to spend up to 25% of your gross monthly income on housing expenses. Most home loan programs require two years of consecutive employment or consistent income, either with the same employer or within the same field.

Get Daily Mortgage Rate Updates & News

It really is essential to talk to a lender to find out all the first-time home buyer loan options you can qualify for. Getting pre-approval on a loan is a great first step toward buying a home. It may feel overwhelming, but that’s when using a trusted mortgage lender like Mares Mortgage can really help. The first thing you will want to do is apply for a mortgage pre-approval. To apply, talk to your lender, and they will assess how much they will lend you based on your income, credit score, and assets.

During pre-approval for a first-time home buyer loan, your lender can also lock in an interest rate. To apply for a grant, you’ll need to find out the qualification requirements for your area because these requirements can vary depending on where you want to buy. Most grants will want a higher credit score of at least 640 and may be limited based on your family size or location. Talk to your trusted mortgage lender to find out if grants are available in your area.

Home Possible Income Limits

This is a sign of stability, indicating that your annual income will likely remain reliable for at least three years after closing on your home purchase. As a first-time homebuyer, you’ll be required to to complete a homeownership education program before your Home Possible application can be approved. Using this tool not only provides you with the area-specific Home Possible income limits, but helps determine what level of financing you’re eligible for. An income of less than 50% of the county area median qualifies you for a Very Low Income Loan.

If you exceed the new income threshold on the Freddie Mac Home Possible loan, Fannie Maes Home Ready loan may be a better option. This program does not have an income limit and allows for lower credit scores. Department of Agriculture are designed to help low- to moderate-income borrowers buy homes in eligible rural areas with no down payment. Unlike FHA and conventional loans, there are no set loan limits. However, strict income, location and square footage limits typically result in maximum loan amounts well below the current FHA and conforming loan limits. The biggest difference is the credit score requirements.

Common Mortgage Requirements for First-Time Home Buyers

Along with normal wages, HomeReady and Home Possible loans also allow borrowers to include boarding income and other income sources in a mortgage application. They allow the inclusion of “non-occupant borrowers” and “non-borrower household members” on a loan. A typical first-time home buyer loan will take about 30 days to be approved. But keep in mind this process can last a couple of months if there are discrepancies or problems with your application. Mortgage approval isn’t one-size-fits-all, so it’s also important to get preapproved for a loan before shopping for a new home. This way, you’ll know how much house you qualify for with your current income.

This announcement has traditionally been a sneak peek at the upcoming lending limits for the Home Equity Conversion Mortgage program. Or, with Freddie Macs Affordable Seconds a second mortgage that can help cover the down payment and closing costs a combined LTV of 105 percent is allowed. Home buyers who earn too much money for Home Possible can access other low down payment loans, including Fannie Maes HomeReady mortgage and the Conventional 97 programs. The Wood Group of Fairway will help you understand your best loan options.

However, you may be able to use other forms of down payment assistance. Fannie Mae and Freddie Mac were chartered separately by Congress in 1938 and 1970 before being spun off into shareholder-controlled companies. Currently, they’re government-sponsored entities under the Federal Housing Finance Agency. Although founded at different times, they have a shared mission of providing mortgage funds that are affordable for the general public. According to Freddie Mac’s requirements, you’ll need a FICO score of 660 or higher to qualify for a Home Possible loan. Planet Home Lending is an approved Freddie Mac Home Possible® lender.

Homebuyer education is required for first-time buyers. The USDA doesn’t set a minimum score, but USDA-approved lenders usually require at least a 640 score to qualify. The maximum DTI ratio the VA will accept is 41%, according to VA guidelines. However, lenders may approve a loan with higher DTI ratio if the residual income is at least 20% above the guideline. The VA calculates how much extra money is left over in a veteran household after standard paycheck deductions and a maintenance expense calculator based on the square footage of the home. The result is called “residual income,” and the amount required varies based on where you live and the size of your family.

If you do qualify, your level of income will further indicate how much of a down payment you’ll be expected to provide. The amount of interest your lender attaches to the loan is also impacted by your level of income. For example, you could qualify for an Affordable Second – a secondary loan from a nonprofit group or a state or county agency, giving you access to more funding. Buying that vacation home will cost you more every month after Fannie and Freddie added significant markups to the pricing lenders can offer on second home mortgages. Buying a two- to four-unit investment property can be a quick way to earn multiple streams of rental income from a single property. The USDA nearly always requires an appraisal, and does not offer any appraisal waiver options for purchase loans.

In fact, there are several other mortgage programs that offer low down payments. In some cases, you might be able to avoid a down payment altogether. An individual can use these programs multiple times as long as they meet the qualifications.

No matter the home type, you must live in the property as your primary residence. This program is not for second mortgages or investment homes. In fact, it is only for first-time homebuyers, which Freddie Mac considers anyone that hasn’t owned a home before or those that have not owned a home in the last three years. It’s a government-sponsored enterprise designed to keep money flowing to mortgage lenders so that those lenders can provide mortgage loans to borrowers who want to buy homes. Freddie Mac does this by purchasing loans from lenders to replenish their supply of funds. For any mortgage, lenders will take a close look at your debt-to-income ratio to determine whether you can afford monthly payments.

Since income levels and home prices vary greatly across the country, the Home Possible eligibility guidelines for income fluctuate, based on zip code. To qualify for the Home Possible program, the combined income of all borrowers must not exceed 80% of the area’s median income. A typical Home Possible buyer will receive mortgage rates 0.25 percentage points below todays mortgage rates. Buyers with high credit scores can receive discounts of a half-percentage point. Theyre called Refi PossibleSM and RefiNow1, respectively. Additionally, the property needs to be owner-occupied by at least one of the applicants on the loan, and a minimum FICO credit score of 660 is required for all loan applicants.

Other requirements to qualify for a mortgage

Please contact your tax adviser for any tax related questions. Home Possible loans are an excellent way to get a foothold in the world of real estate, as long as you can qualify. The income limits on these loans, however, might negate some of the advantages that come with this agreement. Unlike some mortgage product options, Home Possible loans allow you to apply with a non-occupant cosigner.